The following article was produced by Professional Planner and sponsored by Metrics.

The best private credit managers aren’t just good at originating and structuring deals, they’re good at managing loans to repayment, of which a key part is sometimes working with underlying companies to turnaround performance.

Occasionally, it requires taking control of a company or enforcing rights under security agreements—an integral aspect of managing private credit portfolios.

This has played out in the media recently, with a number of non-bank lenders being forced to take control of companies that have defaulted on loan payments.

The heightened attention on private credit reflects the increasing acceptance and popularity of the asset class, particularly among wholesale investors.

It also highlights a need for more education around the benefits and risks of investing in private credit, according to Andrew Lockhart, co-founder of Australian private markets funds management group, Metrics Credit Partners.

“Private credit is a relatively new asset class for many investors to gain access to and there’s a lot of misinformation in the market,” he tells Professional Planner.

“This type of activity has been going on inside the banks forever. The only difference is that when people invest in a bank deposit, banks are incentivised to pay them as little as possible on that deposit to generate a return for shareholders but, in private credit, managers are incentivised to manage risk and deliver returns to investors.”

Established in 2011, Metrics has a proven track record of performance and the required skills and experience to assist companies through difficult periods, according to Lockhart.

He points to the group’s recent takeover of a site previously held by a Melbourne-based developer, after it defaulted recently on a loan which Metrics originally funded in 2022.

As part of the deal, Metrics’ debt-only investors were fully repaid and ownership of the company’s asset was separately acquired by Metrics’ hybrid debt-equity funds.

“We lent that company $41 million against a property based on an independent ‘as is’ valuation of $67 million and when it defaulted, we exercised our security and after following appropriate recovery processes, we eventually moved to acquire the asset for around $50 million, which was the total amount owing to us,” Lockhart says.

“Shareholders and the subordinated or mezzanine debt providers have unfortunately lost the money they invested, but we plan to develop that project and anticipate to deliver a 20 per cent return for our investors.”

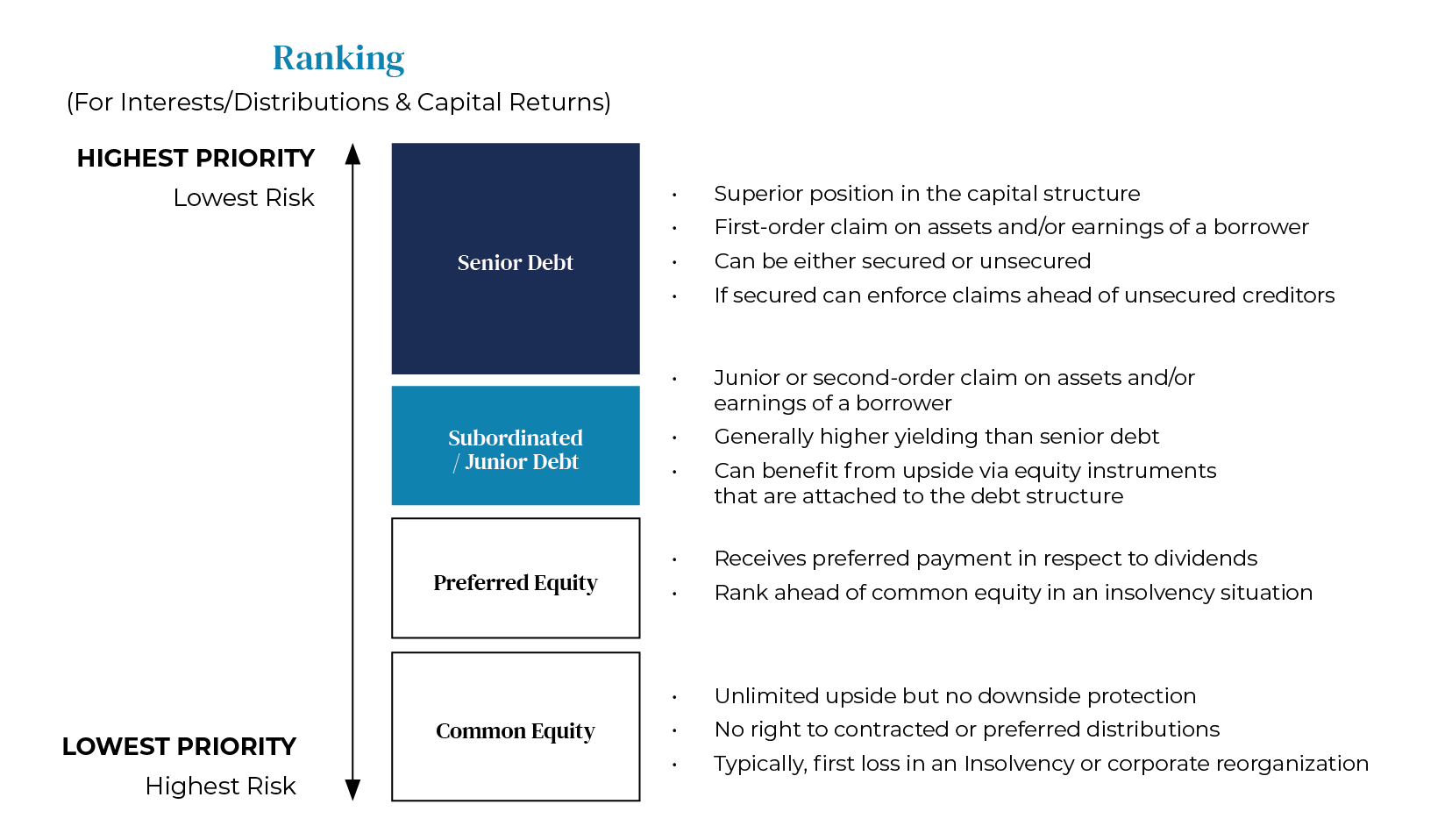

Lockhart says it is important for investors to understand a company’s capital structure and where they sit in the pecking order, emphasising that senior secured debt in the capital structure of a company ranks in priority and is lower risk than equity ownership.

Senior debt position in the capital structure

The pecking order

Within the private credit universe, there is a broad and deep mix of assets, with varying degrees of risk.

Some display defensive characteristics, such as senior secured debt, and can serve as an alternative to traditional fixed income, bonds and hybrids. Other higher yield assets, such as unsecured subordinated and mezzanine debt strategies or debt with equity linked performance rights can generate higher total returns and serve as an alternative to equities.

For this reason, Lockhart says private credit can play a dual role in a portfolio.

It can form part of an investor’s defensive allocation and also be an important source of alpha.

It depends on the risk appetite of the investor and the managers ability to originate and structure transactions at different parts of the capital structure. The differentiation via appropriate investment product, mandate and disclosure of the investment strategy is required to ensure a proper fit for investor portfolios.

“If you are a senior secured lender providing debt and the company or project is generating sufficient cashflow to service and repay debt, then you’re in a lower risk position,” Lockhart says.

“Even if you’re providing a subordinated or a mezzanine loan then you are taking more risk than the prior ranking senior secured lender but lower risk than the equity investor. That is, shareholders’ equity is at risk and must be lost before either lender is exposed to the risk of losing money.”

On a risk-adjusted basis, private credit investors can potentially achieve equity-like returns without equity-like risk by moving along the risk spectrum, Lockhart says.

“In cases where challenges arise, it is often due to the higher-yielding nature of the investment which inherently carries a greater risk of default. In such cases, the manager still has options to effectively manage the exposure and safeguard investor capital ,” he says.

Fake news

Lockhart claims certain segments of the market have a vested interest to paint every troubled transaction in private markets as private credit, evidenced by the portrayal of AustralianSuper’s investment in education software provider, Pluralsight.

While private credit and private equity are often closely linked, AustralianSuper originally made an equity co-investment in Pluralsight, and appear to have also provided equity by way of a subordinated shareholder loan.

Ultimately, Pluralsight’s lenders ended up taking control of the company.

“Ownership of Pluralsight, where equity investors believed there was initially substantial equity value has unfortunately been lost and the business ownership and control transferred to lenders for effectively zero consideration. This loss of equity value created the loss and had nothing to do with private credit,” he says.

“The shareholders’ capital has been wiped-out but the private debt providers haven’t lost a cent. They own the company and if the business then goes on to generate earnings growth, these lenders stand to profit from the growth in value of the company but the original shareholders will not benefit.”

Lockhart is keen to dispel the myth that “in bonds and in debt there’s an asymmetric risk” and if a company defaults, the value of an investment goes to zero.

Again, he cites the Melbourne transaction, where the company defaulted but Metrics investors did not lose their capital given they converted the value of one asset, that is the loan, into a new asset, being the full ownership of the property asset with no debt outstanding.

“If we lend $50 million to a company and the share price drops and it becomes 100 per cent debt, our $50 million represents 100 per cent of the enterprise value,” he says.

“It doesn’t mean we’ve lost capital or any money. The existing shareholders have lost money, but we can convert the value of our debt to equity and have $50 million of value preserved. Now we’re in a position where we can participate in the company’s potential future earnings growth and success, which may ultimately increase the value of the investment.”

Despite Lockhart’s positive assessment on company’s defaulting on their loans, some distressed assets can’t be turned around.

While private credit can deliver attractive returns, it also carries risk.

It is inevitable that some companies will face difficulties, impacting the ability of managers to pay distributions, which is why manager skill is so critical.

Most investors allocating to private credit strategies consider these to be defensive portfolio allocations and are looking for income.

Equity investors, on the other hand, are typically seeking exposure to high growth companies and out-sized returns.

To satisfy the different needs of different investors, large, experienced private credit managers can manoeuvre transactions to deliver appropriate outcomes, Lockhart says, pointing out that, in the case of the Melbourne property transaction, Metrics’ debt-only investors were fully repaid and the asset was acquired by the manager’s hybrid debt-equity funds at the distressed asset value.

“We’ve created different funds with clear risk and return objectives, so investors understand the parts of the capital structure that they are exposed to,” he says.

To have and to hold

Lockhart says that, turnaround stories aside, when it comes to private credit, most of the hard work is done upfront in the underwriting stage to minimise the risk of loss. In private markets, credit is generally a hold-to-maturity proposition, making it even more critical for managers to conduct robust credit analysis and due diligence on companies. Managers must originate deals, structure transactions with the appropriate terms, conditions, covenants, and take security and stress test scenarios on future cashflows; all to protect investors and minimise the risk of loss but also to generate returns.

Leave a Comment

You must be logged in to post a comment.