On Wednesday this week and last, CoreData and Professional Planner hosted roundtable discussions with the heads of leading financial planning licensees, at which CoreData presented some top-level findings from its 2016 Licensee of the Year research.

The 2016 research sets a new benchmark: CoreData received more than 1500 responses from financial planners, practice principals, risk specialists and accountants providing advice. Many of them were Professional Planner readers who responded to invitations to participate in the research.

In total, a dozen licensees were walked through the research – some of it quite confronting – that delves into how the licensees are perceived by their own advisers, and how advisers perceive the quality of support and development their licensees provide.

The depth of even the top-level findings means that only a fraction of it could be covered in the 90-minute roundtables, and even less still can be covered here. More detail – plus additional insights gleaned from CoreData’s current shadow shopping exercise – will be presented to delegates at the Dealer Group Summit, on June 6 & 7. (It’s still not too late to register.)

At the summit we’ll also be naming the 2016 Institutionally Branded Licensee of the Year, Institutionally Affiliated Licensee of the Year and the Independently Owned Licensee of the Year, as well as the overall 2016 Licensee of the Year. Finalists were announced yesterday.

Ultimately, all financial planning licensees are grappling with two really big issues: first, how to deliver more high-quality advice to more Australians; and second, where to find the planning resources – financial planners – to do that.

The CoreData research has some revealing things to say about the penetration of financial planning in the Australian community. It estimates that out of a total population of 26 million, roughly 11 million people could benefit from financial planning services. In coming to that conclusion, CoreData suggests that anyone earning more than about $80,000 is a potential customer.

Obviously, if that threshold is raised (or lowered) then it changes the potential market, and the penetration rate. Be that as it may, the number of people who actually use a financial planner is about 2.68 million – about 24.3 per cent of the potential market. What of the rest?

Communication is everything

About 18.6 per cent of the available market has used a financial planner in the past and would use one again. The most common reason they give for not currently having a planner is startling: the one they had simply stopped communicating with them.

A further 14.2 per cent of the potential market has had a financial planner in the past, but a bad experience means they will never have one again. About 22.3 per cent has never had a financial planner and say they will never have one – these tend to be the so-called “controllers”, who believe, rightly or wrongly, they’re capable of doing everything themselves. And about 20.6 per cent has never had a financial planner but would be happy to talk to one.

So of the available market, 24.3 per cent already has a relationship with a financial planner, and CoreData says another roughly 30 per cent isn’t really interested or simply won’t use one; consequently about half the available market is still contestable.

Not one prone to overstatement, CoreData founder and principal Andrew Inwood suggests that “if any other marketplace existed in the world where half the market available to you wasn’t being penetrated, you’d consider that you’d failed”.

The CoreData figures accord with the conventional wisdom that only about one in five people who could benefit from a financial planner’s services actually use those services. The bigger question is: why?

It’s convenient to blame a range of external factors: media coverage; political interference and legislative upheaval; poor investment markets; the stars. But the CoreData research suggests that there is a range of factors, each of which can be totally controlled by the industry, which are also major contributors.

The reason we know this is because of the wildly different experiences people have when they visit a financial planner. If the systems, processes and delivery mechanisms underpinning delivery of financial planning were consistently applied and effective, then client experiences should be roughly consistent. No one is suggesting that every planner should offer the same services, nor that they should have a common value proposition. But the clients’ perception of the experience of visiting a financial planner should be consistent. And it’s not – not even remotely.

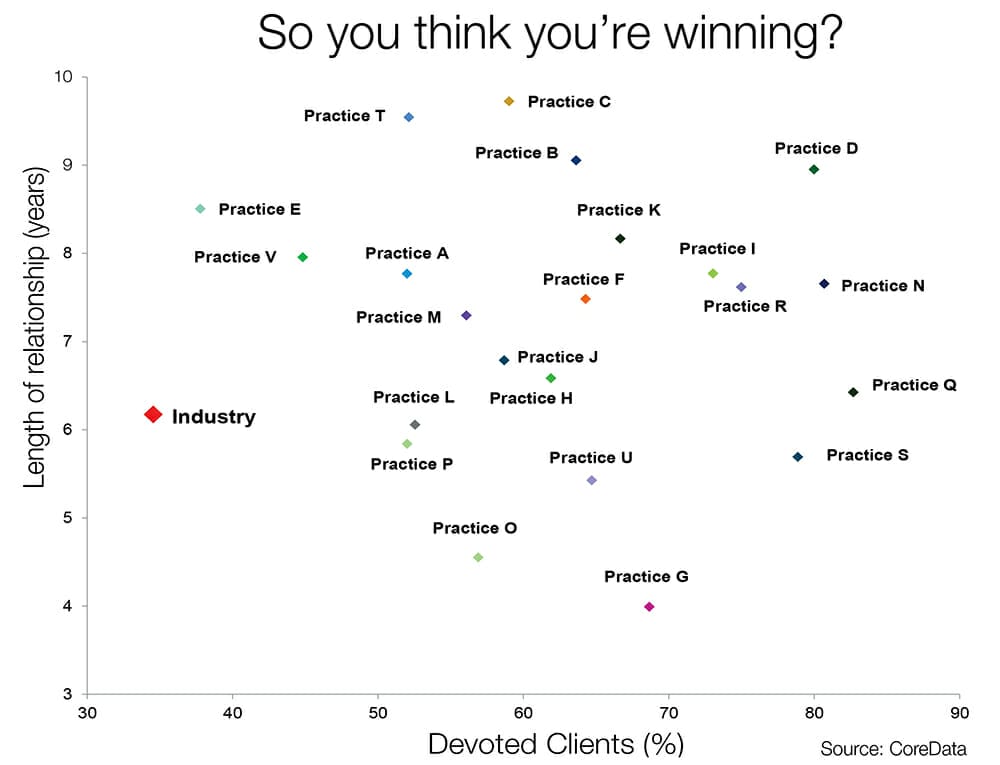

The chart below illustrates the issue. Take a moment to contemplate it. It maps out how many “devoted” clients 22 financial planning practices have, against how long those clients have been with the relevant practice. A “devoted” client is one who loves their financial planner and the experience of dealing with the planner. There is value attached to devoted clients, because they will tend more to refer others, and they are more likely to buy more services.

Totally devoted to you… (the planner)

One way to interpret the chart is to say well, yes, it stands to reason that client experiences vary from practice to practice because each practice has a different philosophy, systems, processes and access to products and services. That would be a fair conclusion, except in the chart, every practice represents the same licensee.

So even though the licensee works hard (as all should) to implement consistent and robust advice systems and processes, and to provide financial planning practices with equal access to and opportunities for support and development, the way financial planning services are experienced by clients is still massively variable across the licensee’s practices. This is a problem.

The scattered experience is part of what is holding back the industry from achieving better penetration of the available market. “While we’ve got this going on, there is no penetration,” Inwood says.

CoreData says that as an industry, financial planning remains “challenged” when it comes to delivering consistent experiences to customers. And there is a low correlation between the length of the relationship and the proportion of devoted clients – which means the experience doesn’t necessarily even improve over time.

The factors causing this, and some of the solutions, should be high on the list of things to address for many licensees. Improving the client experience – by first making experiences consistent – is a critical step in the journey towards increasing the proportion of Australians who benefit from using financial planning services.